Financial markets hate uncertainty, and few things breed uncertainty quite like all the possible outcomes of a war.

Time and compliance restrictions make it so this forum can’t possibly provide a thorough analysis of the situation, nor could I use this space to walk through each limb of the decision tree that the markets and investors will navigate.

What I can and will try to do is highlight some major themes, provide a little perspective, and invite you to give me a call to go into greater detail and reposition these general thoughts into specific terms for you and your situation.

Before I get too far along, please let me express gratitude and extend well-wishes to anyone who may have a loved one directly involved in or impacted by these events. Thanks to every veteran and current military member who has taken risks most of us couldn’t ever comprehend. No matter where we each may stand on the decisions made to engage in military activity, I’m sure we all share the hope that each of the men and women who carry out their orders would return home safely. Likewise, we all would surely share the view of a tragedy for any lives altered or lost, military and civilian alike.

War is a form of hell on earth. While my role is to manage assets and assure retirement and estate plans through these seasons, far be it from me to pretend the stresses that work through the financial markets compare to the stress felt by those and their loved ones on or near the true front lines.

Shifting attention now to the markets, war is again a form of hell. I’ve been in this field of work for 32 years now, so I’ve seen my share of war or warlike seasons; many of them centering on the Middle East. Of course, longer wars with more economic impact have been fought throughout American history, but to think this operation in Iran will eventually rise to the level of those historic events is very unlikely for a host of reasons.

That doesn’t mean, however, that this will fade quickly and not leave a negative mark on the US and global economy. In truth, after a month or so to this point, we’ve already seen damage to the economy and a renewed expectation of inflation mostly owing to $100+ oil prices.

On the flip side, we all know how quickly oil can move in both directions; meaning it could shed a lot of value in short order if we do see some progress on the opening of the Strait of Hormuz or with a clearer picture on supply replacement from other places.

This fact introduces quite a conundrum for the financial markets. With even a modest degree of improvement (meaning a decline) in oil prices, there will come a wave of optimism that the worst is over for the economy and, therefore, the financial markets. Keep in mind, too, that markets bottom before the news turns positive. In fact, FundStrat’s Tom Lee shared a few statistics today on CNBC that bear this out. He analyzed the last 8 major geopolitical conflicts and found that the stock market typically bottoms very early in the war. On average, the market low occurs about 1/3 of the way into the conflict’s total duration. In several cases, the bottom happened within weeks of the war starting, long before the war itself ended.

These historical facts make it difficult for those that want to run to the hills and leave the markets.

Sure, if we knew exactly how long this war would last, we’d be able to draw a lot more from Tom’s points. Even without the end date, though, I think the point is still clear. Markets quickly begin to price in negative scenarios, and they don’t have much use for thoughts about what could go right. History shows us that by the time the news flows are still negative and the war is ongoing; stocks have often already started recovering. But before we turn that corner, fear takes over and selling is indiscriminate. Investors of all sizes – institutions, sovereign wealth funds, pension managers, retail mom and pops alike – all sell whatever they can or feel they need to for the immediate fear to be assuaged. This is the reason diversification shows relatively limited benefits when looking through a very short-term lens. In highly emotional times, selling almost always precedes analysis. In the fullness of time, however, diversification works. Every time. While there are brief periods where assets that are in no way related will move as if they are business partners, they don’t last. Assets that are supposed to zig while others zag ultimately do. The process just takes a little time.

A saying I like quite a bit is to “invest as if your future is watching”. It implies your ‘real’ future, not just next month. This mantra helps endure the occasional period in which apples and oranges are lumped together, so to speak.

Our emotions are not our allies when it comes to investing, that’s well documented. The more we fret over current headlines, the less likely we are to fully benefit from the better days of the future. The more we predict what will come next, the more power we give to the element of luck. This is not to suggest, in any way, that we don’t adhere to discipline. Quite the opposite, in fact. This is a point to emphasize the need to plan rather than predict. The value of a plan, for everything from how to be allocated, how and when to add or reduce market exposure, and how to order portfolio distributions to have the most tax efficient and secure retirement and estate plan is absolutely critical. Without these types of plans, our emotions have much more room to run and lead us to ruin. With these plans, we can maintain the perspective needed to endure difficult periods in the market, whether they are caused by geopolitical or more fundamental events.

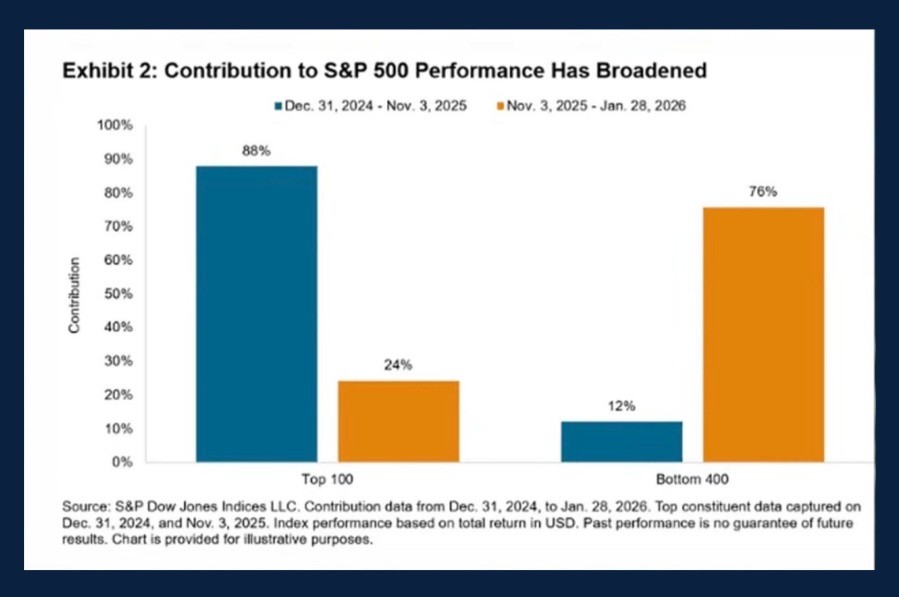

I’d like to take a moment to quickly point out something happening within the market that has been mostly overshadowed by current events. I’m referring to the long-awaited virtuous rotation from the past leaders, mostly the mega-cap tech companies, into the rest of the market. I’ve written time and again about how good it would be to see this cascading effect of money trickling down from the top

throughout the rest of the market components. This began to happen late last year, and it was picking up steam before the war began. I believe that when the focus moves away from the war, this trend is likely to continue, at least to a fair degree. It’s a little dated, but this chart shows what I’m referring to:

This broadening reflects a healthier market backdrop and it is something we’d like to see continue.

Lastly, in a recent issue of Worth Considering (click here to read), I highlighted the fact that the 2nd year of Presidential terms are historically the most volatile and produce the smallest gains. They also tend to serve as connection points between the stronger phases of that same cycle. They don’t highly correlate with deep or long-lasting market dives, they are just bumpy sections of a historically safe journey. My base case is that’s largely what to expect from 2026.

Whether it’s war or any other worry, market corrections always have a scapegoat. Sometimes they are legitimate and other times they are merely coincidences. I’d say this Iran war is a legitimate piece of the current correction puzzle. I’d also say I think it’s unlikely to be the cause of a recession or bear market.

As such, investors are best served by enduring it rather than getting too skittish or clever trying to either dodge it or game it.

And that’s particularly probable given the unique risk at play now which is the Showman In Chief, Donald Trump. Like it or not, we are in a world where we are always one tweet away from a new paradigm. The President’s preferred communication styles serve to exacerbate the market’s natural inherent volatility. Again, this presents a real challenge for those who may want to take an overly negative stance in the markets. One pre-dawn tweet could reverse the course of a bearish portfolio and paper profits in negatively oriented bets could turn ugly before anything could be done about it.

As an asset class, stocks are more than likely in the midst of a perfectly healthy correction. They are likely to find their footing before much longer if the news about the war suggests true progress, even in the absence of a full

scale cease fire. On the other hand, if the President’s forecasted timeframe for this exercise is proven to be off base, a bear market scenario comes clearly into play. While this extended war scenario needs to be fully understood and accepted, I don’t think it is the most likely outcome and shouldn’t be anyone’s expected base case for a forecast ahead.

In other news, I’ve added a new face to my personal Mt. Rushmore of non-traditional investment icons. Welcome Leonardo da Vinci to the scene!

He is next to the three other unexpected icons – Yogi Berra, Dr. Seuss, and Mike Tyson.

These enigmatic men don’t take the place of true investment legends like Warren Buffett or John Templeton, but they have each taught me very useful lessons from their unique perspectives.

The baseball star Yogi Berra is known for his own brand of ‘wisdom’. Brilliant sayings like “it’s déjà vu all over again”, “you can observe a lot just by watching”, or “Nobody goes there anymore. It’s too crowded”. His Yogi-ism’s should serve as warnings to investors that you’ll hear some profoundly stupid things when it comes to financial markets, economic forecasts, or wild and reckless blathering from pundits on TV or the internet. It’s best not to take a lot of what you hear as true genius or valuable insight of any sort.

Author Dr. Seuss is a hero in the investment landscape because of how he chose to illustrate his children’s books. No straight lines. The connection to success in the investment world is obvious. If you expect straight lines, you’ll be sadly disappointed and surely not perform well as an investor. Far better to understand that curvy lines and zig zagging patterns are part of the story and, if kept in proper perspective, will help investors along their journeys.

Mike Tyson is perhaps my favorite because he seems like the least likely person to teach lessons on anything in the field of finance. Not true! His most famous phrase is a gem that applies directly to both boxing and investing: “Everybody has a plan until they get punched in the mouth.” Here again, the connection to success in the investment world should be obvious. When the markets inevitably pop us in the mouth from time to time, do we have a plan we can rely on? And will we have the discipline to adhere to it?

This is a great introduction to why da Vinci is now on my list. To one of the most respected minds and accomplished men throughout history is attributed this quote: “Simplicity is the ultimate sophistication”.

Simplicity is a scarce commodity in my field. My world of investment management, retirement, and estate planning is rife with people making things complicated. There’s no room for shortcuts in these fields, so the actual work behind the scenes can often be complex, but the end result for the client should be as simple to understand as possible. Instead of cloudy, ambiguous language or wishy-washy guidance, da Vinci’s brilliance reminds us that if something is made too difficult, it isn’t likely to get done. As an advisor, the more plainly spoken I can be and the more concise the plans my team and I can lay out for our clients, the better. Again, this doesn’t mean the plans and the advice aren’t backed by every bit of research necessary. My aim is to take this cue from da Vinci and make things as simple as possible for our clients to understand and ultimately achieve.

Welcome the team, Leo….slide over a bit Yogi.

As we head into Holy Week, regardless of how you express your faith and beliefs, let’s not lose sight of the fact that some things are far more enduring than financial market volatility. Faith, hope, love; kindness, compassion, friendship – these are things that will be with us forever and truly enrich our lives regardless of the current news cycle or market mood swing.

With this in mind, the team and I wish you a blessed Holy Week and invite you to please give me a call if you have any questions or concerns about these current market conditions, or anything else for that matter.

The Takeaways:

- This period of volatility is almost certainly not yet over. Swings in both directions will likely happen and will be driven almost entirely by the war; more specifically, the price of oil at any given time.

- It’s my opinion that a correction that both lasts longer and pulls markets down a little further would be healthy. Ironically, if this is the path of the coming weeks, the months and years to follow look better. I’m not cheerleading for a dip and I’m not in the bear market camp, but markets need to be shaken out occasionally to ensure value and avoid bubbles.

- There’s little reason to believe financial markets here and abroad won’t be higher in the years to come. There is no evidence of the type of systemic risk that leads to serious economic damage or deep bear markets.

- This 2nd year of the Presidential cycle isn’t likely to be a strongly positive year in its own right, but it will hold up just fine and connect us to a stronger phase ahead.

- Effective investing means ignoring noisy “wisdom,” accepting market volatility, staying disciplined when plans are tested, and prioritizing simplicity in strategy and communication.

Disclosure

Securities offered through International Assets Advisory, LLC (“IAA”) – Member FINRA/SIPC. Advisory services offered through International Assets Investment Management, LLC (“IAIM”) or Global Assets Advisory LLC (“GAA”) – SEC Registered Investment Advisor(s). IAA, IAIM, and GAA are affiliated entities.

The information provided is based on carefully selected sources, believed to be reliable, but whose accuracy or completeness cannot be guaranteed. Any opinion herein reflects our judgment at this date and is subject to change without notice. This should not be construed as an offer or solicitation to buy or sell securities. This information is not intended to be legal or tax advice. Please consult a tax, legal, or financial professional with questions.

Investors should consider the investment objective, risks, and charges and expenses before investing. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be either suitable or profitable for a client or prospective client’s wealth management investment portfolio. Past performance is not an indication of future performance. International Assets Advisory, LLC and its affiliates, employees and/or directors may have positions in these securities, and may as principal or agent, buy from or sell to customers. All securities are subject to price and yield change and subject to availability. Investments in securities and insurance products are: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE. Stocks, options, and mutual funds are subject to market volatility and may lose value. Mutual funds, Unit Investment Trusts and Variable Annuities are sold by prospectus only. Please read the prospectus carefully for important information about fees and risk considerations. Bonds are subject to changes in interest rates, risks of defaults by issuer, and the loss of purchasing power due to inflation, or the risk that an issuer will be unable to make interest or principal payments. Additionally, bonds and short-term investments entail greater inflation risk than stocks. Any fixed-income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Investing in securities underlying in currencies other than the U.S. dollar involves certain considerations comprising both risk and opportunity not typically associated with investing in U.S. securities. The security may be affected either favorably or unfavorably by fluctuation in the relative rates of exchange between currencies, by exchange control regulations, or by indigenous economic and political developments.